Part Two: Choosing a Target for Regular Investing

Regular investing is simple, direct, brutal and effective. However, in addition to depending on the ability of the practitioner to earn money outside of the market, it depends even more on the selection of a quality investment target. If a mistake is made in the selection of the target, the result over the long term will be terrible.

It's important to note that what we are discussing is "how regular investors should choose an investment target", and not "how investors should choose the correct investment target". The former is a subset of the latter, and actually only has one additional condition:

Is it worth holding over the long term?

In the investment world, the Greet letter alpha (α) is used to refer to returns that exceed overall market returns. The goal of regular investors when choosing their investment target is to create alpha. They won't sell before at least two full market cycles have passed, because to do so would be to waste all of their previous efforts. All they do is buy, so they won't know for a long time whether or not their alpha is positive or negative.

2.1 Investing Advice That You Can Blindly Follow

The hardest question for those just entering the market is this:

Which one should I pick?

How can someone who doesn't even know what their criteria should be make a choice? How can someone who can only see the superficial and not the true nature of something make a correct choice about what to hold over the long term without wavering? There is a simple, direct, brutal and effective strategy that is also free:

Blindly follow the advice of truly successful investors who have shown excellent returns over the long term.

"Blindly follow" sounds extremely terrifying, but we actually can blindly follow the advice of truly successful investors who have shown excellent returns over the long term (please notice the key term: "long term"), because in the investment world there is an amazing phenomenon:

The more long-term successful experience investors have, the more open they are.

Warren Buffett started writing public letters to investors a long time ago, and later on he continued to share his investing ideas and decision-making process on television and through other media. Starting in 1964, Buffett has written a public letter to investors each year. As of 2019, he has been writing them for 54 years! Ever since 1973, he and Charlie Munger have held freewheeling Q&A sessions at yearly shareholder meetings. In 2019, the 46th year, a record 16,200 people attended, not including people watching online around the world.

Berkshire Hathaway's shareholder letters from 1977 to 2018 are available here:

http://www.berkshirehathaway.com/letters/letters.html CNBC's website has a special section called the "Warren Buffet Archive": https://buffett.cnbc.com/warren-buffett-archive/

Warren Buffett's mentor, Benjamin Graham, was also someone who shared without reservation. In addition to teaching investing classes, he wrote several books, most notably Security Analysis (1934) and The Intelligent Investor (1949). Warren Buffett read The Intelligent Investor when he was 19, and he became a fan of Benjamin Graham. One Saturday in 1951, while in the library of Columbia Business School, Buffett learned that Benjamin Graham was Chairman of GEICO, and he immediately decided to pay a visit to the company's office. Many years later, in an interview with Forbes, Buffett recalled that the investment he made in GEICO at the age of 20 was one of the investments he was most proud of.

Joel Greenblatt's investing returns are perhaps even more impressive than Warren Buffet's -- from 1985 to 2006, his annual compounded returns exceeded 40%! Having been successful over the long term, Joel Greenblatt is also quite willing to openly share. He has published three books, namely You Can Be a Stock Market Genius (1999), The Little Book That Still Beats the Markets (2010), and The Big Secret for the Small Investor (2011). He is so down to earth that his standard for writing the books was that his teenage children could understand them.

Greenblatt didn't just share his ideas in his books, he also made a website, Magic Formula Investing, that allows investors to use his ideas to build their own portfolios. All you have to do is enter a few parameters and the site will give you a ready-to-go portfolio based on the "Magic Forumula".

Ray Dalio, the founder of Bridgewater, is yet another investor who has been successful over the long term and is willing to share his ideas. Long before his book, Principles, was officially published in 2017, he released a version for free online. In 2019, he even released an app called Principles in Action, which helps readers put the principles in his book into practice.

In the investing sphere, one must use money, time and action to create real results, and everyone is either a 0 or a 1. Investors who can successfully produce returns over the long term are 1s, and the rest are 0s, including those so-called experts who spend all of their time yelling through the television or other media but have no skin in the game. Investors like Warren Buffett, Joel Greenblatt and Ray Dalio don't need to spend all day screaming through the television, because their ideas have already been clearly expressed through their books, writings and speeches.

Perhaps the most simple, direct, brutal and effective strategy that novice investors can use is to just buy whatever Warren Buffett buys. They don't need to dream about "beating Warren Buffet", they can just “keep up with Warren Buffett" by buying shares in his companies. The easiest way to do this, of course, is to just buy Berkshire Hathaway shares. If novice investors feel that Berkshire Hathaway's share price is too expensive (it was over $310,000 in October of 2019), then they can look at its individual holdings and choose the stocks they want!

CNBC has a page listing all of Berkshire's stock holdings:

Of course, if a novice investor actually did this, their success would be dependent on whether they were able to hold the stocks for as long as Warren Buffett does. For the vast majority of people, holding for the long term is a much bigger challenge than making the initial choice of what to buy.

Alternatively, they could go to Joel Greenblatt's Magic Formula Investing site, enter a few parameters, and buy the suggested collection of stocks. It's important to note, however, that Greenblatt's Magic Formula is not suitable for regular investing, since his method is to choose a new batch of stocks each year. See? Regular investing isn't the only effective strategy, it's just the easiest for most people to put into practice.

So why can we blindly follow these truly successful investors who have shown excellent returns over the long term? It's because they have used their own strategies over the long term, and their strategies have passed the test of time. They are also skilled at thinking with a long-term perspective, or else they wouldn't have been able to carry out their strategies over the long term. In their eyes, the long-term effectiveness of a strategy is not related to how complicated it is. To the contrary, only simple strategies can actually be carried out over the long term. Furthermore, the long-term effectiveness of a strategy is not correlated with the intellect of its user. The core prerequisite for the long-term effectiveness of an investment strategy is whether or not it is faithfully carried out over the long term.

In fact, there is no secret to success. Even if there were, it would be an "open secret". All paths to success are open, as are all of the necessary tools and knowledge. It's just that few people are able to patiently follow a path, picking up knowledge and understanding bit-by-bit, and persistently execute along the way. How few? They're actually quite hard to find.

These people are the rare ones who have achieved a unity of knowledge and action. Actually, the suggestions of anyone in any field throughout history who has achieved a unity of knowledge and action are worth accepting and putting into practice. If we understand it right away, that's great, just do it. If at first we don't understand, we can blindly follow.

The key point is that investing ideas from the most successful investors are free! You don't even need to worry that these ideas will be adopted by everyone and lose their effectiveness, because history has shown that the vast majority of people won't use these ideas. Maybe it's because most people are afraid of simplicity. They think that success is difficult, so they must discover a complicated secret or they won't be able to succeed. There's also another important and common fear involved that keeps people from following this priceless advice: it's terrifying to use our own money to carry out the ideas of others that we still don't understand!

Of course, there's yet another reason:

People like to use their own smarts and efforts to get a reward.

"Even if I make money by buying whatever Warren Buffet buys, it doesn't feel like success." This might be the actual feeling that many people are hiding.

2.2 Value Investing and Trend Investing

When people talk about value investing and trend investing, they often mistakenly see them as opposites. In fact, they are only opposites when viewed from a short-term perspective.

For regular investors, however, who always view things from a long-term perspective, value investing and trend investing are not opposites. In the long term, which is to say after two full market cycles, value investments will show a trend of compound growth, and investments that trend upward over the long term will also certainly be valuable. A simple change in perspective can cause the relationship between two terms to be completely opposite!

I often say the following:

Don't have blind faith in value investing.

I also often say this:

Don't have a one-sided understanding of value investing.

Why do I feel that I always have to remind people of this? Because I often see this situation:

Most people are clearly (short-term) trend investors, because the bull market was obviously the reason they entered the market! But as soon as they get trapped by falling prices in a bear market, they suddenly become value investors!

So, in most situations, people who mention the concept of value investing to you actually only became value investors after getting trapped in the market. I can also guarantee to you that, once the market picks up, they will suddenly turn into what they would call trend investors.

This is truly a fascinating phenomenon. They completely fail to understand that the huge loss and the awkward situation that they are facing are entirely due to having a different perspective. Even sadder is that these people, who use the short term as the basis for their decisions, also don't know that they have no way of understanding the free and correct advice on the market that is available from those most successful investors who can be blindly followed. And it's all due to a different perspective! Because those "truly successful investors who have shown excellent returns over the long term" all look at things from a long-term perspective.

To take it a step further, trend investing is better than value investing when viewed from a long-term perspective.

Even though Benjamin Graham's value investing thesis is obviously correct, few people notice that it has a hidden limitation:

According to his thesis, you must always pay attention to the current price.

Behind this hidden limitation is an even more deeply hidden factor:

Even though it is possible to determine whether the current price is lower than the current value, it's nearly impossible to determine the future price and value, especially the price and value after two full cycles.

It's an almost impossible feat to both pay attention to the details of the present and seriously consider everything that could happen in the distant future. This is the key reason why truly successful value investors are so rare. A good analogy is the saying that if you wear one watch you'll basically know what time it is, even if it's a few minutes slow or a few minutes fast, but if you wear two watches you'll be very mixed up.

According to value investing theory, you must work hard to find an investment with a price below its actual value. But when will you sell it? According to the theory, once its price exceeds its actual value you should sell it, whether it's been ten days or ten years since you purchased it.

Following this theory, even Warren Buffett will make mistakes. His most famous mistake was his investment in Disney -- he actually made two mistakes trading Disney stock. In 1966, 36-year-old Buffett met Disney founder Walt Disney in California. Following the meeting, Buffett bought 5% of Disney (NYSE:DIS) for $4 million at a price of $0.31 per share.

Note: Historical data is from Yahoo Finance (DIS), and the chart above was created in Google Sheets; you can view the data and chart here.

In his 1995 investor letter, Buffett relayed this story. He bought Disney stock in 1966 at $0.31 per share, and then sold it a year later for $0.48 per share, making a profit of 50%. Over the next thirty years, Buffett could only watch as Disney stock rose, reaching $13 in 1995.

But the story was not over. In 1995, Buffett helped Disney purchase Capital Cities/ABC, of which he was a shareholder, and once again ended up with a 3.6% stake in Disney! He sold his shares within three years, though, and missed out as Disney's stock continued to rise up to $129 in October of 2019. Business Insider calculated that, had Buffett continued to hold 8.3% of Disney through 2019, his shares would have been worth $21 billion, and he would have received $1.5 billion in dividends.

Of course, this story doesn't mean that Buffett failed in his investment, and he certainly didn't actually "lose" $22.5 billion. After all, he made a profit on Disney, and he didn't just spend the money after selling -- he kept investing according to his strategy, and he has a 55-year track record of around 25% returns. Over the past 53 years, not accounting for dividends, Disney has returned just over 19% compounded annually. If dividends are taken in to account, Buffett would have been better off holding Disney, but he certainly didn't "lose" as much trading Disney as some people think.

What this story really tells us is that, over at least two full cycles, value investing, which requires constant focus on price, is not necessarily better than long-term trend investing.

Therefore, regular investors focus more on the overall trend. Even though we are also value investors, the difference is that we view things from a long-term perspective. While it can make people uncomfortable, the logic is sound:

If the correct trend is chosen, then while the difference between price and value is not unimportant, it's not as important as people think.

With a focus on long-term trends, and the requirement of only focusing on the long term, regular investment targets must be chosen in a different way. Compared to many other investors, regular investors have an extra screening criterion:

Sustained growth over the long term.

Don't discount the importance of "one extra criterion".

Amazon (NASDAQ: AMZN) currently has the highest market cap of any e-commerce company in the world. According to Morningstar's calculations, it has provided investors with a compound yearly return of 40.42% over the past five years. Over the past 15 years, the compound yearly return has been 28.51%.

Have you thought about why Amazon started by selling books, even though there were so many other potential items to sell? Aside from the fact that the book market is a large market, and the fact that people need and want to buy books frequently, there is one extra screening criterion that the book market fulfills: once you have sold a book, you very rarely need to provide customer service. Just this one extra criterion eliminated 99.99% of the other choices!

Regular investors can only choose investments that grow sustainably over the long term (of course, the more growth the better!). Just this one seemingly simple criterion eliminates 99.99% of the options, because, strictly speaking, there is no one individual investment that we can be sure will meet this criterion, no matter how good it looks now. This is because companies are just like people:

In the long run, we are all dead. -- John Maynard Keynes

So what should a regular investor do?

2.3 A Long-term Perspective and Macro Observation

Everyone can understand how difficult it is to pick the best possible investment, especially in the midst of price fluctuations. It's as difficult as a world champion archer standing on a boat being rocked by waves in the middle of the ocean hitting the bullseye on a target on the shore.

Only investing in one investment also entails opportunity cost. Time and money are limited resources, and if you use them in one way you can't use them in another. So, if you invested in A but B performs better, the opportunity cost of your investment decision is quantifiable.

Fortunately, we have another simple, direct, brutal and effective solution:

Invest in everything.

This sounds a little bit crazy, and perhaps a bit stupid, but let's put aside whether it's actually crazy and/or stupid, and first ask: Is it possible to invest in everything? The answer is definitely yes! The MSCI World Index tracks the price of 1,650 mid- and high-cap stocks in 23 developed countries. If we actually invested in this index, what would our results be?

Note: It's possible to buy ETFs that track various world stock indexes. The iShares MSCI World ETF (NYSEARCA: URTH) tracks the MSCI World Index; the iShares MSCI ACWI ETF (NASDAQ: ACWI) tracks the MSCI All Country World Index, which includes emerging markets; and the Vanguard Total World Stock ETF (NYSEARCA: VT) tracks the FTSE Global All Cap World Index, which also includes developed and emerging markets.

In addition to the MSCI World Index, there are several other MSCI indexes, including the MSCI Emerging Markets Index. From December 31st, 1987, to September 30th, 2019, the MSCI World Index has shown yearly compounded returns of 7.86%, and the MSCI Emerging Markets Index has shown yearly compounded returns of 10.37%. This makes sense, as you would expect emerging markets to grow faster, albeit with more risk.

An investment in a fund that tracks the MSCI World Index is like a bet on the growth of the world economy, and an investment in an S&P 500 fund is like a bet on the US economy. If we look again at the chart of the S&P 500, we can see that it has also provided around 9% returns over several decades!

Note: The historical figures above are from Yahoo Finance (^GSPC), and the chart was created in Google Sheets; you can view the chart and data here.

Investing in the S&P 500, with an annual compound growth rate (ACGR) of 9%, performed better than investing in the MSCI World Index, which had an ACGR of 7.86%, but the MSCI Emerging Markets Index performed even better, with an ACGR of 10.37%. What's the easiest way to explain this?

- The US grew faster than the world;

- emerging markets grew faster than the US.

Now we can see that, when we choosing investments, in addition to "one" (quite dangerous) and "all" (mediocre), there is another choice: "part". So which parts are worth choosing? I like this analogy even better than "betting on the world":

Choosing investments is like choosing a method of transportation. If you walk, you can still get there, it will just take longer. But if you have a bike you shouldn't walk, if you have a car you shouldn't bike, and if you have an airplane you shouldn't drive -- you should take whatever will get you there the fastest.

We've seen that emerging markets develop faster, so it's easy, we can just choose the "emerging market part", right? Or could we just choose one fastest-growing country, or even just choose the fastest growing industry in that country? Sure! Choosing a market that is growing faster is just like choosing a faster method of transportation.

It's extremely difficult to pick the best investment out of tens of thousands of possibilities, but it's quite easy to pick a couple of the fastest-growing areas out of ten or so regions. Everyone knows that the US and China are the fastest-growing places in the world. If I were to design an ETF, I would look for my investments in just these two places. This ETF would have a high probability of doing better than the MSCI World Index, wouldn't it? To take it a step further, it wouldn't be that difficult to further limit my investments to the fastest growing one or two industries in each country. At least legendary investor Masayoshi Son doesn't think it would be difficult:

Making money is easy. All you need to have done is invested in the Internet 20 years ago, because at that time the Internet was the future of the world. Now, you should invest in AI, because AI is the future of the world.

I agree with Masayoshi Sun's point of view, and believe that in the foreseeable future AI will be the best industry. However, my point of view is slightly different. For instance, I believe the following:

No matter how good the algorithm is, it needs data to feed it. Public companies with large and growing amounts of user data already have sufficient profit-making ability. If in the future algorithms are large trees, then growing amounts of data are fertile ground. Without fertile ground, the trees can't grow. Most algorithm companies will in the end be used by large companies with data.

When I started to buy lots of bitcoin in 2011, many people thought I was crazy. They all said the same thing: "Isn't it too risky?" They felt like it was too risky, but I had the opposite feeling:

Isn't it too risky not to invest in Bitcoin?

This was the logical reasoning behind this feeling:

We've seen the incredible changes brought about by the Internet allowing information to flow rapidly with basically zero cost, so what kind of incredible changes would be brought about if assets could also flow rapidly with basically zero cost?

After ten years, the Internet is still bringing about massive changes. Even if it isn't exactly what we initially imagined, it's still amazing. In the same way, ten years from now the financial Internet is extremely likely to have brought about incredible changes, even if we can't know exactly what those changes will be...

So for me at the time, blockchain was the future, blockchain was a trend, and blockchain would likely be the fastest growing industry. Looking back from eight years later, it has become the fastest growing industry, and my investment has grown at a scale not even imaginable at the time.

You see? "Choosing the fastest growing sector" is the most simple, direct, brutal and effective method. It's also the most direct conclusion that can be derived from macro observation. For those who can't think based on the long term, this statement isn't understandable as an effective piece of advice. To them, it seems stupid, and you can imagine them yelling out, "Who doesn't know this!?" Yes, everyone knows this, but not everyone thinks based on the long term, so they are not used to macro observation, and so of course they can't understand the power of long-term macro observation.

Can we take it further, and ask ourselves, "Can I choose the fastest growing company in this fastest growing sector?" I don't think it's worth it, because doing so is essentially returning to the most dangerous situation, and becoming more vulnerable to regression to the mean. The core skill of macro observation is very simple: don't go to extremes. The reason is that we hate risk, and we hate systematic risk even more. The core strategy is always "a part of a part":

- Look for one or more regions in the world;

- in those regions look for one or more sectors;

- in those sectors look for the best companies...

However, whether we're choosing regions, sectors, companies or projects, we should never pick just one. So in a global sector such as blockchain, as long as opportunities are available, my choice is no longer a single investment, but the mix of investments in BOX, which includes BTC, EOS, and XIN.

The diagram below may make it easier to understand.

The largest circle represents the entire world, and you are standing in the middle holding a bow and arrow....

You look around, hoping to find the best place to shoot your arrow. It's difficult, because in the entire circle there are limitless places to chose, and it's basically impossible for you to choose the best possible place and hit it from so far away...

So you think about it, and you choose "everywhere". You decide to change tools, and trade your arrow for a net. This is much better! It's easy, and even if the results are average, it's much better than shooting arrows all day and hitting nothing...

But you'd like to have better results, so you first choose a general direction. You're not just choosing randomly, you have a reasonable basis for your choice: you decide to shoot your arrow in the direction of the area that is developing most rapidly. This way you're more likely to hit something, right? Or you could put down your arrows, and just throw your net in that direction!

But then you realize that you could use the same basic rationale to adjust your general direction. If there are regions that are growing more rapidly, then there must also be sectors within those regions that are growing the most rapidly. The same logic still works.

You've already made three guesses: 1) a net might work better than an arrow; 2) certain regions might grow more rapidly than the whole; and 3) some sectors within those regions might grow even more rapidly. If you keep guessing, your accuracy will certainly suffer. So what should you do? Don't use an arrow, use a shotgun! This way, although your accuracy will suffer, you'll be more likely, and perhaps almost certain, to hit something. Anyway, since it's so far away, no one can be completely accurate, but after so many adjustments, you're more likely than others to be accurate!

In the end, you have another discovery, which is that using an arrow is never the best choice...

Choosing a mix of multiple investments, rather than just one, has a powerful effect. The most famous example once again comes from Warren Buffet. In April of 2017, United Airlines had a PR disaster on their hands when, after overselling a flight, they had 69-year-old David Dao dragged off of an aircraft. Quite a few of the media reports that followed were about Warren Buffett, because he owned a large amount of stock in United's parent company. The reports said that, since the company's stock had gone down 4%, losing more than $1 billion in market value, Buffett had lost more than $90 million. At the end of trading that day, the stock was down just over 1%, so Buffett's paper loss was around $24 million.

But did Buffett really lose money? No. In addition to United, he also had stock in American Airlines, Delta Airlines, and Southwest Airlines. The stock prices of those three airlines all went up that day, giving Buffett an overall paper gain of $140 million on his airline stocks! Buffett's diversification in the airline sector insulated him from the price volatility of a single airline stock. Had Buffett not had diversified his holdings in the airline sector, the result would have been quite different!

2.4 Major Trends All Have Bubbles

Words that have been paired most frequently with "bubble" include "tulip" and "Internet". In 2019, a new one has been added: "Artificial Intelligence". People are worried that that a global AI bubble is about to burst, even though just a year ago startups in the AI sector were the hottest in the world. On October 5th, 2018, Forbes reported that there were 14 AI unicorns just in China (a "unicorn" is a startup with a valuation of over $1 billion). In aggregate, these companies had valuations of over $40 billion. A year previously, AI startups had been even hotter, with a report from Tsinghua University stating that 369 investments had been made in AI startups in China, with the total investment reaching $27.7 billion.

But why are people suddenly worried about a bubble? It's because there has been a rash of negative news stories about the AI sector. For instance, it was reported that Facebook infringed on user privacy in order to develop their voice recognition system, and that IBM used similar methods to develop their facial recognition system. AI has also been used for what some consider to be nefarious purposes, such as in the case of Cambridge Analytica's use of Facebook user data in the US elections, and Amazon's use of AI to fire low-productivity workers.

Perhaps the silliest story was about Kiwi Campus, a startup founded at UC-Berkeley in 2017 that makes robots, called Kiwibots, that deliver food on campuses. It has received multiple rounds of funding, and its CEO received an entrepreneurship award from MIT in 2018. In the summer of 2018, however, it was reported that the "AI robots" were actually being controlled remotely by students in Columbia being paid $2 an hour.

The AI sector seems too hot. With startups raising too much money, unclear valuation methods, and frequent issues with applications of the technology, it's hard not to be reminded of the Internet bubble. So, of course, people start to worry that there may be an AI bubble that could burst...

But is it such a bad thing for a bubble to burst?

Let's take another look at the historical price chart for the S&P 500. The two red circles indicate the peak of the Internet bubble in 2000 and the peak of the housing bubble that led to the financial crisis in 2008. If we were living in the world of 2000 to 2003, it would seem to be a terrible winter for the Internet, with companies going bankrupt and dissolving. From our vantage point in 2019, however, we can see that from 2000 to 2019 the Internet grew from being the world of a few to being everyone's world. According to the World Bank, in 2000 only 1.8% of people in China were online; by 2019, WeChat -- just one app -- had over 1.1 billion users. This is the story of the Internet in China -- from 1.8% of the population using the Internet to 70% of people using just one app in around 20 years. Long-term trends can take a while, but they are quite powerful!

For regular investors, even if we entered the market at the height of the bubble in 2000, looking back after two full cycles, in 2015, our entry point still looks like a "low" price. It turns out that the secret to "buy low, sell high" is quite simple:

Wait for a long time after you buy before you sell.

So is the popping of the AI bubble a good thing or a bad thing? It's hard to say for others, but for regular investors a bubble popping is always a good thing. In fact, the popping of a bubble may be a great opportunity for a regular investor to enter the market.

If we look back over history, industries representing all great trends went through bubbles. The difference between the tulip bubble and the Internet bubble was that, while tulips were not completely without value, there was no way for their value to grow sustainably. The Internet, however, had a value that could grow over time. All the way through the Internet bubble the Internet was growing, creating value, and changing the world.

Why do all great trends go through bubbles? The best explanation comes from John Fisher's Transition Curve:

When going through a transition, after some initial anxiety, people feel happy because they think that, "At last something's going to change!" But then they often begin to experience a myriad of negative emotions. Some people deny the negative emotions, and then crash later on, while some slowly fall into feelings of fear, guilt and even depression. While some eventually give up, others slowly begin to accept and adapt to the change. But this only happens after a long process.

Major trends, which become apparent after many years, must initially go through the process of acceptance described above. The first crest in the curve is the cause of the bubble, and the ensuing trough is the reason for the bubble bursting. This is shown most clearly in the markets, because the market price at each moment is a representation of everyone in the market's collective understanding of an investment. When people are feeling disillusioned, the bubble pops.

So, contrary to what most people think, the popping of a bubble quite possibly represents opportunity. Whether or not there actually is an opportunity depends on whether or not the object of the bubble has long-term sustainable value and growth potential. If it does, then there is an opportunity. It's possible, though, that bubbles may continue to occur until its value has been fully realized.

After reaching an all-time high of $19,800 in December of 2017, bitcoin entered a long bear market. As of October 2019, it remains in a bear market, with its price less than 43% of its all-time high. But is the popping of this bubble different from the popping of previous bubbles in the bitcoin market? From its inception through October 11th, 2019, bitcoin, the world's first blockchain application, was pronounced dead 337 times. Each short bull market has been called a bubble, and they have all popped, but the popping of the bubble in 2017 has one difference from previous bubbles:

No one denies bitcoin's value.

This is an extremely important, if subtle, difference. I have a very simple, direct, brutal and effective way to determine if a trend has been established:

Don't look at how many people have already accepted it, look to see if most people can no longer deny it.

Undeniability is an important sign of an established trend. It doesn't matter whether or not they understand it, or whether or not they accept it. If they can't deny it, then the trend has basically already "filled up the bubble". This is the best signal for regular investors to decide when to enter the market. This is why I didn't introduce BOX, my no-carry, no-management-fee blockchain ETF, until July of 2019, even though my thinking about and designs for a blockchain ETF began in 2015.

It's important to point out that most novice investors fall into the trap of "looking for the next...". Actually, very few people succeed by choosing carefully and holding over the long term (whether through regular investing or not), and the vast majority of people never make deep macro observations from a long-term perspective, but everyone is jealous of those who have already succeeded, so they can't help but think:

If only I had also chosen correctly that early!

But it's hard for that thought not to evolve into this next thought:

I also want to find an investment that I can get in early on!

This is a dangerous thought, especially for novice investors! The problem is, the more of a novice one is, the stronger this thought is. Just ask yourself, have you had this thought? Then ask yourself again, didn't you have this thought as soon as you started investing? Doesn't this thought always make you feel anxious?

There are lots of details that those who are about to fall into this trap don't know. For instance, there are actually very few major trends that will really change the world. Also, if a new major trend does appear, it will probably be years from now, rather than right now or in the immediate future. More importantly, the development of a great trend that has already been identified will continue for a long time with increasingly rapid growth. Actually, "this one" is much more realistic than "the next one".

If we're able to grab on to one major trend in our lifetime, we're already very lucky!

2.5 The Trend Within the Trend

Choices are the most important thing, especially in investing. If we review what we've gone through so far, we have already made many choices:

- One or everything (global)

- The best parts (regions)

- The best parts of the best parts (sectors)

- A combination of the best investments in the best parts of the best parts

It's a lot of decisions, but they are easy to summarize. All of them are decisions about trends. Not choosing just one investment, but stepping back and choosing to invest in everything, is done in order to reduce risk and keep up with the global trend. In this case, alpha is zero. Choosing the best parts of the whole is done in order to find the parts that are developing the fastest, and in doing so create positive alpha. Choosing the best parts of the best parts is done to create even higher alpha by following trends. Finally, choosing combinations of investments in the best parts of the best parts is pursuing the same goal: first reduce risk, and then see if it is possible to increase alpha.

In order to choose our combination of investments, the most simple, direct, brutal and effective principle is this:

Match the sector's development trends.

Below, I will take BOX as an example, because it is a combination of investments that was chosen through this process.

Risk Warning

The strategy of regular investing is objectively correct, but it is impossible to remove subjective judgment from the choice of investments for regular investing. So the choice of investments for regular investing is the responsibility of each investor. Each investor must use their own money and time over the long term to take responsibility for their own choices. Please be cautious.

This section is primarily about why, in July of 2017, I chose BTC, EOS, and XIN to be the initial components of BOX, and it necessarily contains some of my own subjective judgments. You must use your own objective understanding of the objective world to choose your own investments.

Conflict of Interest Notice

- I am a long-term holder of BTC (from May of 2011)

- I was an angel investor in BlockOne, which developed EOS (initial investment in May of 2017; all shares sold in 2018)

- I was an angel investor in Mixin Network (October of 2017)

After eight years of observation, thinking and practice, I think that blockchain technology has a development path that is slowly becoming apparent:

Trusted ledger (BTC) → Trusted platform for code (ETH/EOS) → Trusted execution environment (Mixin) → Trusted hardware (?) ...

Bitcoin was the world's first blockchain application. At its core it is an open, transparent, immutable, distributed, trusted ledger. Projects such as Ethereum and EOS, which came along later, have the goal of becoming a blockchain application platform, which is to say that application code can be written to and executed on an open, transparent, immutable, distributed, trusted ledger. Putting a ledger on a blockchain allowed for a trusted ledger, and putting application code on a blockchain allowed for trusted code. Mixin Network combines a Trusted Execution Environment (TEE) and a Directed Acyclic Graph (DAG) to create an open, transparent, immutable, distributed digital asset storage network, or a trusted execution environment. Maybe in the near future we will also see trusted hardware.

There is one final reason why I chose these investments. From inception until they are widely accepted, almost all technologies go through the following three stages:

Inception → Adoption by businesses (2B) → Adoption by individuals (2C)

From this perspective, EOS is a blockchain platform for businesses, and Mixin Network's first dApp, Mixin Messenger, is a platform for individuals. One of Mixin Messenger's most important components -- in fact it is a base-layer feature of Mixin Network's public chain -- is a distributed, multi-coin wallet with the best user experience in the industry.

Furthermore, these three investments have reached the "undeniable" stage. Of course they haven't been accepted by everyone, but no one can deny their value. This is the best time for regular investors to enter the market.

In January of 2021, more than 500 days after the establishment of the BOX Regular Investing Group, the components of BOX were adjusted for the first time. Currently BOX includes seven components:

- BTC

- EOS

- ETH

- DOT

- MOB

- UNI

- XIN

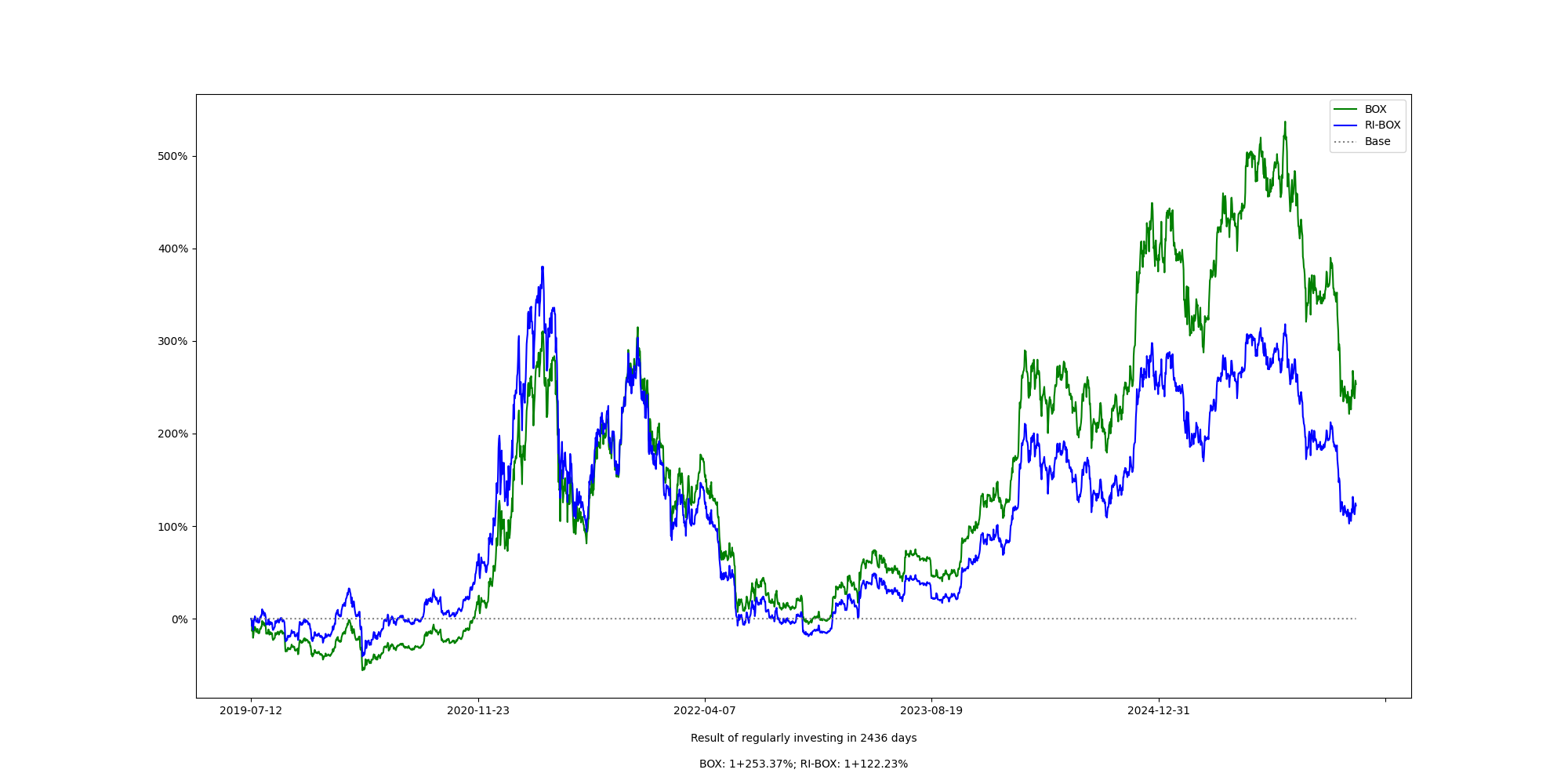

At this point, BOX has evolved into a rather mature "Digital Assets Index ETF". The following chart shows the returns on BOX from July 12th, 2017:

There has long been debate in the investment world about whether alpha -- results that beat the market -- actually exists, even though rare investors such as Warren Buffet, Joel Greenblatt and Ray Dalio have consistently beaten the market over the long term. There's a joke that shows the silliness of blind adherents to "efficient market theory":

A student saw a hundred dollar bill on the ground and exclaimed to his professor, "Look! Is that a hundred dollar bill?" The professor didn't even deign to look, saying, "That's impossible! If it were really a hundred dollar bill, somebody would have picked it up a long time ago."

If the market were 100% efficient, then alpha could not exist. The problem is that, if we look at any given moment in the market in isolation, it's 100% inefficient. Price and value sometimes matching up doesn't mean anything -- even a broken clock is right exactly twice a day! If we put all of the individual moments back together, then over the long term the market should be efficient, but how long is long term? No one knows. If we look at it from the perspective of a regular investor, after two full cycles, the variance between the current price and the historical price at any given moment will seem even greater.

Obviously, I believe that alpha exists, and I'm always thinking about how to find better strategies to create it. If you do well, alpha is positive; if you do poorly, alpha is negative. As a regular investor, your final results can be described by the following formula:

p = δ + α - γ

p represents your final performance. δ, or delta, the fourth letter of the Greek alphabet, represents the performance of the overall market. γ, or gamma, the third letter of the Greek alphabet, is borrowed from a concept introduced by Morningstar in 2013. My definition of gamma, however, is slightly different. Here, gamma refers to returns that you would have gotten if you hadn't made mistakes. This is an extremely important and interesting concept, and it is one of the core concepts explored in Part Three of this book.

β, or beta, the second letter of the Greek alphabet, refers to the correlation between your returns and overall market returns. When beta is 0, they are completely uncorrelated. For instance, if you "regularly invest in US dollars", then your returns will be completely uncorrelated with the stock market. When beta is 1, your returns are 100% correlated with the market. In our equation, p = δ + α - γ, delta is equivalent to a beta of 1.

For regular investors, all alpha comes from careful decisions that are made before starting to invest. Regular investors are lucky in that once they start investing they don't need to worry about things like choices, adjustments, or other issues that keep other investors up at night.

As you have seen, the choice of investments for regular investing doesn't require many tactics or smarts. As long as you get the process basically right you should be okay. However, the difficult part of being a regular investor is that even before you start you have to be sure that you have made your choice and will stick with it over the long term. This is probably the best example I can come up with of how something can be "simple but not easy".